U.S. Companies Can “Be the Bank” with ReserveLending+

Firstly, we would like to take a moment to remind folks that the unFederalReserve Forum is the best place to respond to this and other articles.

To schedule a ReserveLending+ Demo, click here.

Introduction

The time has come as our institutional DeFi product is finally in an alpha testing phase, and will very soon be ready for demo’ing to any U.S. based entities holding crypto on its balance sheet.

Today’s article will break down:

- What is ReserveLending+

- Security and the Compound protocol

- The Role of the RIA, BD or Bank

- ReserveLending+ Compliance and Custody

- Our First Registered Investment Advisor (RIA) Licensee

- ReserveLending+ Reporting, Analytics, and Monitoring

- How ReserveLending+ Benefits $eRSDL Holders

- RL+ conclusion

Now, drop your anchor ⚓, and let’s get started!

What is ReserveLending+?

ReserveLending+ is an institutional DeFi (decentralized finance) ecosystem and P2P (peer-to-peer) lending platform that empowers companies to optimize their net cost of capital onchain. Excess Bitcoin, Ethereum or USDC can earn interest at greater savings rates than offered by traditional banks and loans can be drawn at competitive rates for qualified borrowers.

The platform is without intermediary, allowing qualified participant entities to self-custody their WBTC, ETH or USDC until a peer borrower is identified and its loan funded.

You can read about our latest development updates on ReserveLending+ and what the platform will look like in our recent Dev unWrapped article.

All loans are overcollateralized. The borrower’s collateral is drawn down to pay the lender’s interest. Lenders are largely protected from borrower defaults (though it is not riskless by any means) due to this overcollateralization and the existence of a programmable, automated bot that pays off loans without sufficient overcollateralization.

In the August 2021 Consensys report on institutional DeFi adoption, the author points out the Maslow hierarchy of needs equivalent in this space. Let’s cover how RL+ meets these needs:

Security and the Compound Protocol

Tremendous growth has occurred across decentralized versions of lending and borrowing platforms, prediction markets, margin trading, payments products, insurance, and more. The DeFi ecosystem now represents an expansive network of integrated protocols and financial instruments worth more than $70B.

Our core software is a fork of the DeFI protocol, Compound. From the WealthSimple article entitled, “What is Compound”, a concise description is as follows:

“Compound is “decentralized”, which means … that [it] is “non-custodial”, unlike a bank or a crypto loans company (such as BlockFi). This means that nobody, not even Compound’s creators, can access your crypto. What’s yours is yours.”

Vaultoro explains the importance of Compound’s non-custodial aspect in this article:

“Compound Finance is intriguing because existing crypto-asset holders can earn interest without giving up control over their funds. Serving as a non-custodial solution is paramount in this industry. If you do not control your cryptocurrency wallets’ private keys, you are not in any position of power. DeFi intends to empower users; thus a non-custodial approach is mandatory.”

It is important to note that we selected Compound because the version of the protocol we used has not been hacked in 3 years+ of operation, and has had trillions of cumulative value run through its core in that time period. The Compound protocol, as well as our fork of that contract, has been subject to numerous security audits. It is simple, elegant and allows for us to wrap an interface around it that is intuitive and easy-to-use.

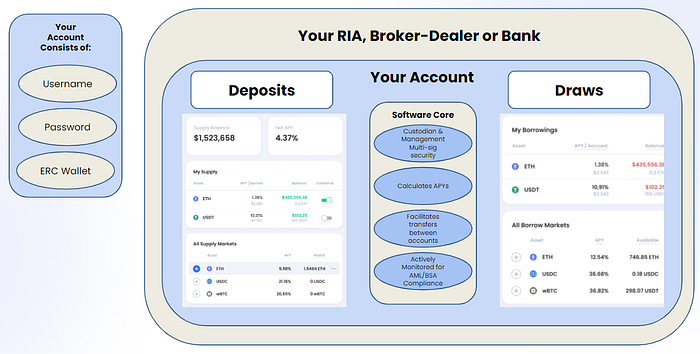

The Role of the RIA, BD or Bank

There are four parties to the platform:

- Us (aka. Residual Token Inc.) — the fintech and management services provider that built the platform, handles any required integrations with the Host, inputs the settings, monitors User (aka. Host’s customers) activity, reports User activity as required by the Host or regulator. We also help find Users for the Host, assist with onboarding and advocate for the Host.

- The Host — The RIA, Broker-Dealer or Bank that licenses the software from Us. There are three considerations: Technology, Operations and Business Development. From the technology perspective, the Host provides the brand and style guide to Us so that we can match the User’s current experience with the Host. The Host provides us information on their KYC tracking system (e.g. KYC Chain, spreadsheet, Securitize, etc.) so that our software can properly gate entry to only those entities that are approved customers of the Host. From an operations perspective, the Host’s customary onboarding procedures remain unchanged. If the Host wants balances from the platform reported on a consolidated User page, we will work with the Host to make sure that information is available. This is the extent of Host’s responsibilities as a qualified, third-party custodian (“Custodian”) bears the atomic-swap moment custody risk possibly present in the software. From a business development perspective, the Host continues to offer its standard product suite with this one just being an additional reason why Users should choose your RIA, BD or Bank to do business.

- Custodian — an SEC qualified custodian will have administrative access to the core smart contracts comprising our software. No changes to the core contract may be enacted without their approval and the rules for their approval are in line with escrow and custody rules today.

- User — The Host’s customer looking for more banking alternatives, and wants to earn yield on their crypto. They also want the ability to borrow at reasonable rates without waiting.

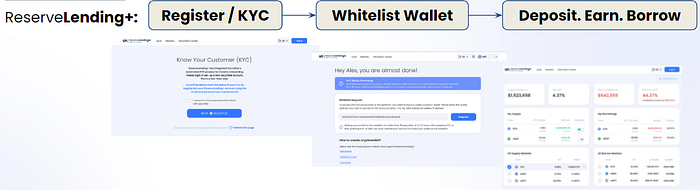

ReserveLending+ Compliance and Custody

Commercial lending and borrowing in the United States is subject to numerous state and federal restrictions and guidelines. Among those include specific Know-Your-Customer (KYC) provisions and Anti-Money Laundering (AML) monitoring requirements. We are FinCEN registered, because even though we are not a financial institution, we wanted the ability to report on behalf of all ecosystem users activity that would be considered suspicious. We aim to exceed FATF guidelines by focusing on what U.S. regulators expect, and based on decades of regulatory experience in borrowing and lending across industries and collateral types.

For KYC, we have partnered with Securitize to offer best in class identity verification, and with over 100,000 identities verified to date; including, 450+ institutions. If you intend to use RL+, you must have a Securitize iD. Apply here today.

Our AML policy can be found here. We use Chainalysis Reactor and an in-house Bank Secrecy Act (BSA) officer to identify and report suspicious activity.

The First Software Host

Lastly, we are looking to partner with an RIA, broker-dealer or bank to provide additional regulatory cover and support. In addition, the target host has access to traditional banking for crypto companies, allowing our customers both access to our DeFI platform and standard savings accounts using fiat at above average saving rates.

We’re also exploring only allowing Gnosis multi-sig wallets to connect with RL+ adding an additional security layer for all RL+ participants. In the mult-sig wallet construct, the entities participating will need dual approval on everything. We’d like to see the community’s thoughts on this requirement, pros and cons in the Forum.

ReserveLending+ Reporting, Analytics, and Monitoring

We’ve spent the last nine months tweaking and improving the customer interface on our retail platform, ReserveLending. Bug bounties and regular public and private QA support are also in place to further ensure we are providing a robust, safe and transparent environment for our users.

Furthermore, we have had multiple security audits performed on the platform, we assume Compound’s existing audits in our own body of knowledge and we expect future planned work by Trail of Bits to close out this phase of our review. A SOC 1 or SOC 2 audit shortly thereafter is not out of the question.

How ReserveLending+ Benefits $eRSDL Holders

Our unFederalReserve technology powers ReserveLending+ and we provide the necessary technical skills, manual operation, and other management functions necessary to ensure a safe environment for those using our software.

For this service and software, RL+’s host will pay a licensing fee to unFederalReserve. This is because, as with the other products made available by unFederalReserve, the host vehicle pays the licensing fee, since they enjoy the revenue that borrowers generate when using unFederalReserve’s bona fide, regulatory compliant rails.

We are using the eRSDL token as a digital marker to track identity, payment and term, in one permission style token! You can read more about Licensing-As-A-Service here. Our procedures call for creating a wallet in the name of the licensee and storing the eRSDL that we purchase out of the market in that wallet. That eRSDL is then trickled out of the wallet at a pace commensurate with the license term into either a long-term storage contract, a burn wallet or will reside untouched in unFederalReserve’s native treasury.

The wallet that token sits in is owned and governed by the Licensor (and not the Licensee). This ensures that the Licensee doesn’t sell their access to the software to a non-compliant third party. However, existence of the token in the public space allows us to develop dashboards, tools and utility that any holder of the licensing token can enjoy without risk of corrupting the token’s original use case.

Licensing fees lend themselves to digital markers. The beauty of smart-contract language is its power to store identity and payment information and contractual agreement information, in this case term, all in one location. Two parties commit to what’s in the code, and the cost of the license is reflected in the count and market price of the token at the time of the Licensor’s acquisition of that token.

Here is an example taken from the LaaS article showing the economic impact of large-scale adoption of unFederalReserve’s software. These are not pro forma estimates of actual expected open market purchases nor an estimate of the value of the token itself. This diagram is meant for illustrative purposes only. No other purpose is intended or implied.

Those boxes in red are cases where the existing supply is not sufficient to purchase tokens out of the market. The buy pressure would likely remedy this, or if the Company extracts all the tokens out of the market, an alternative method (or amount) would need to be considered.

RL+ Conclusion

ReserveLending+ provides U.S. domiciled crypto-native and non-crypto-native companies the ability to optimize their costs of capital, and add utility to their own balance sheet by giving utility to their cash. Balancing costs of capital driven by the amount of capital needed at any given time or excess liquid assets is a key component of hitting KPIs in an environment of increasing people and material costs. We expect ReserveLending+ to address the needs of U.S-based, crypto holding entities and deliver results for the $eRSDL community.